.png)

.png)

The Cost of Waiting for Mortgage Rates To Go Down

Mortgage rates have increased significantly in recent weeks. And that may mean you have questions about what this means for you if you’re planning to buy a home. Here’s some information that can help you make an informed decision when you set your homebuying plans.

The Impact of Rising Mortgage Rates

As mortgage rates rise, they impact your purchasing power by raising the cost of buying a home and limiting how much you can comfortably afford. Here’s how it works.

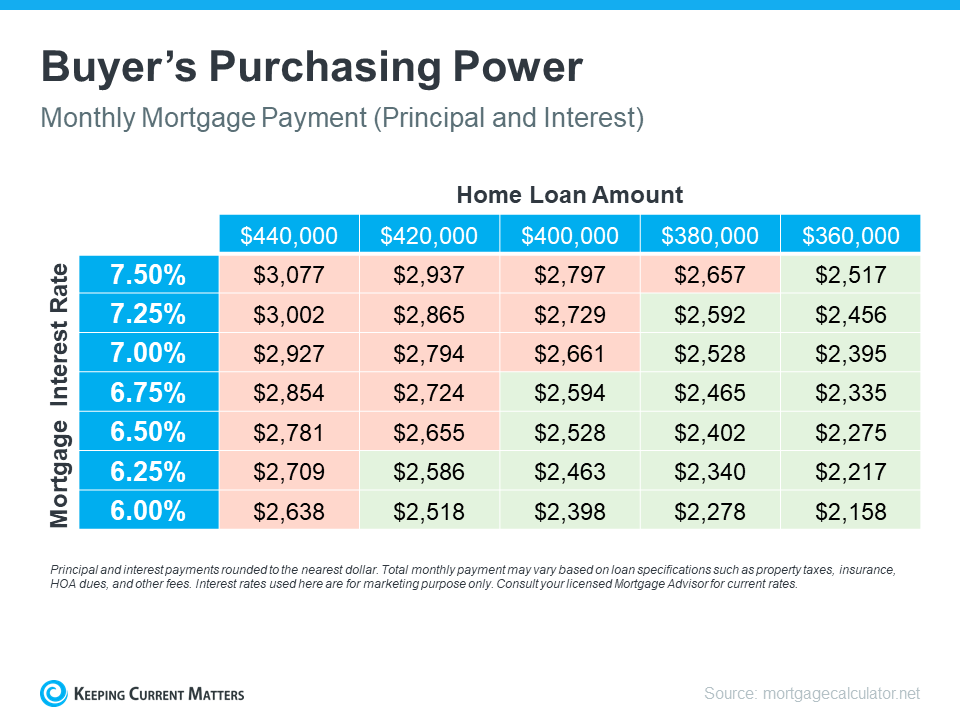

Let’s assume you want to buy a $400,000 home (the median-priced home according to the National Association of Realtors is $389,500). If you’re trying to shop at that price point and keep your monthly payment about $2,500-2,600 or below, here’s how your purchasing power can change as mortgage rates climb (see chart below). The red shows payments above that threshold and the green indicates a payment within your target range.

As the chart shows, as rates go up, the amount you can afford to borrow decreases and that may mean you have to look at homes at a different price point. That’s why it’s important to work with a real estate advisor to understand how mortgage rates impact your monthly mortgage payment at various home loan amounts.

Are Mortgage Rates Going To Go Down?

The rise in mortgage rates and the resulting decrease in purchasing power may leave you wondering if you should wait for rates to go down before making your purchase. Realtor.com says this about where rates could go from here:

“Many homebuyers likely winced . . . upon hearing that the Federal Reserve yet again boosted its short-term interest rates by three-quarters of a percentage point—a move that’s pushing mortgage rates through the roof. And the already high rates are just going to get higher.”

So, if you’re waiting for mortgage rates to drop, you may be waiting for a while as the Federal Reserve works to get inflation under control.

And if you’re considering renting as your alternative while you wait it out, remember that’s going to get more expensive with time too. As Nadia Evangelou, Senior Economist and Director of Forecasting at the National Association of Realtors (NAR), says:

“There is no doubt that these higher rates hurt housing affordability. Nevertheless, apart from borrowing costs, rents additionally rose at their highest pace in nearly four decades.”

Basically, it is true that it costs more to buy a home today than it did last year, but the same is true for renting. This means, either way, you’re going to be paying more. The difference is, with homeownership, you’re also gaining equity over time which will help grow your net worth. The question now becomes: what makes more sense for you?

Bottom Line

Each person’s situation is unique. To make the best decision for you, partner with a real estate advisor to explore your options.

Selling Your Home?

Get your home's value - our custom reports include accurate and up to date information.

Meet Kayleigh Sellars

Born and raised in Columbia SC, I graduated from The University of South Carolina in 2014. Soon after graduating I started my banking career with a credit union. I was able to work my way up and by 2018 managed two markets.

I transitioned to a branch manager role at a large bank and redirected my focus to business and mortgage lending. I was able to see the positive financial impact a home refinance could make for a client and loved walking them through the process. Financial literacy and breaking the process down for my clients are things I’m passionate about.

My free time is spent hanging with my husband, Richard, and our Sheepadoodle, Tucker. Recently my Dad shared a story with me about when I was little and would want to play “mortgage lady”. Here we are now and I’m a mortgage lady! (I promise I wasn’t a weird kid).

803.665.5788